But an AI factory without enough memory is a Formula One car with no fuel tank

Takeaways

-

Micron did not just beat estimates; it reinforced that AI demand is still colliding with a hard physical constraint: memory supply. That keeps pricing power firmly with the producers.

-

The real upgrade is structural. Multi-year take-or-pay agreements, price floors and customer deposits are an attempt to turn memory from a classic boom-bust trade into a more visible cash-flow machine.

-

That makes the fade more dangerous. Betting against Micron now is not simply a valuation call; it is a bet that shortages, hyperscaler spending and customer urgency all cool at once.

-

The risk is that the market begins pricing this as a permanently cleaner earnings model just as capacity eventually catches up. The boom may be real, but memory has a long history of making investors forget where the cycle ends.

Micron’s Blowout

has just turned what was supposed to be a high-wire earnings event into another reminder that, in this AI cycle, the bottleneck is increasingly becoming the business model.

The stock entered results with expectations already pinned to the ceiling. Sentiment was hot, the shares had stumbled over the prior two sessions, and traders were waiting for the usual post-earnings escape hatch: good numbers, great guidance, but not great enough to justify the valuation. Instead, Micron kicked the door off its hinges.

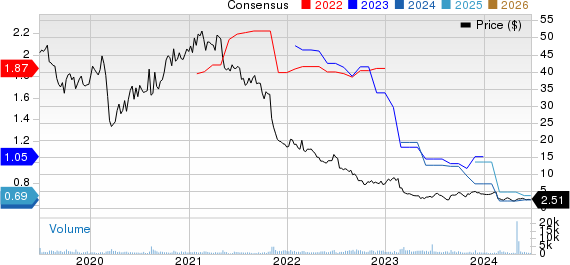

Revenue landed at $41.46 billion against expectations closer to $36 billion. Adjusted earnings came in at $25.11 per share, comfortably above consensus. Gross margins reached 84.9%, while operating margins pushed above 81%. Those are not merely strong semiconductor numbers. Those are numbers that tell you supply is still being rationed, pricing power is still sitting with the producers, and the AI build-out remains hungry enough to swallow every high-bandwidth memory chip that comes off the line.

Then came the outlook, which was even more important. Micron guided fourth-quarter revenue to roughly $50 billion at the midpoint, well above the Street’s $43 billion estimate, while guiding to margins of around 86% and earnings near $31 per share. In a market that has grown used to asking whether AI expectations have become too inflated, Micron’s answer was blunt: demand is not fading; it is outrunning supply.

That matters because memory has moved from being the supporting actor in the AI story to becoming one of its central characters. The market spent the last two years obsessing over the accelerators, the networking stacks, the data-centre buildouts and the hyperscaler capex arms race. But an AI factory without enough memory is a Formula One car with no fuel tank. may still be the engine of the trade, but Micron, SK Hynix and Samsung increasingly hold the keys to the part of the system that determines how fast that engine can actually run.

The real headline, however, sits below the income statement. Micron has now signed 16 Strategic Customer Agreements across data-centre, consumer and automotive markets, covering about 20% of DRAM volumes and roughly one-third of NAND through the end of the decade. These are not loose handshakes made at the top of a cycle. They are multi-year, take-or-pay arrangements designed to lock in supply, protect customer roadmaps and give Micron a degree of revenue visibility the memory industry has rarely enjoyed.

Fourteen of those agreements alone carry minimum contracted revenue of approximately $100 billion through the remaining term, alongside an estimated $22 billion in customer deposits and related commitments. That is a meaningful shift in the memory-cycle playbook. Historically, this has been one of the market’s most notoriously cyclical corners: prices surge, capacity follows, supply overshoots, and margins collapse under their own weight. Micron is now trying to put guardrails around that old boom-bust highway.

The details matter. Price floors within these agreements are designed to preserve gross margins above prior cycle peaks, while ceiling prices give customers more visibility on their own cost base. In effect, Micron is selling more than chips. It is selling supply certainty into an environment where every major AI platform is trying to secure enough memory to keep its infrastructure expansion from becoming hostage to shortages.

That will be the part investors focus on once the initial after-hours fireworks settle. The immediate move higher in Micron is understandable; the company has delivered a genuine beat-and-raise quarter even against elevated expectations. But the more durable question is whether these contracts can transform the valuation debate from a cyclical memory name enjoying a temporary shortage into an AI infrastructure supplier with a more visible and defensible earnings runway.

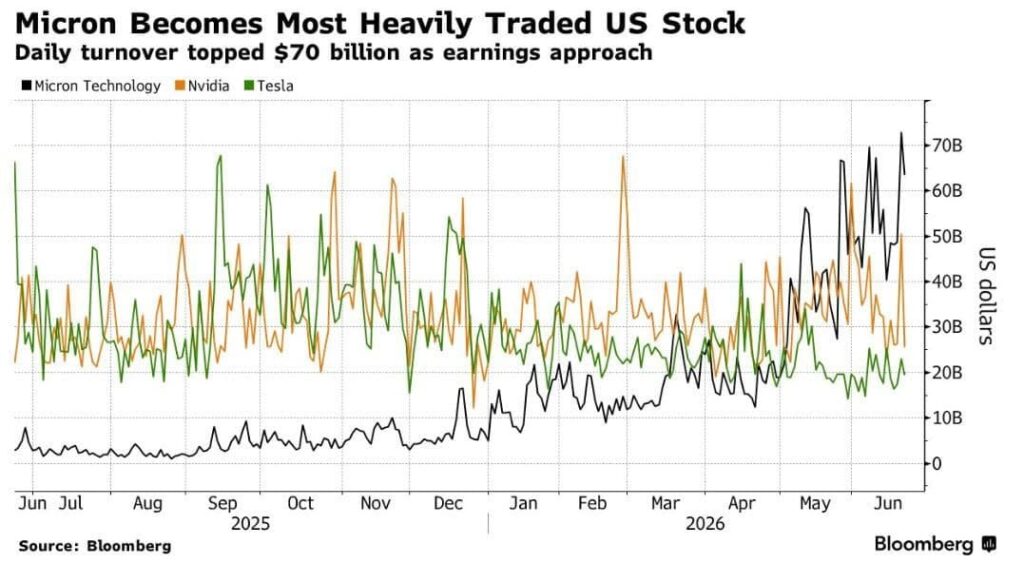

For now, the summer fade-the-rally crowd has a problem. Micron did not merely beat the quarter. It widened the gap between the market’s expectations and the industry’s actual demand reality. The shares had slipped back below $1,000 before earnings, giving nervous longs a chance to question whether the AI trade was finally losing altitude. After the release, the stock ripped more than 10% higher and reclaimed much of that lost ground.

That does not mean the stock cannot pull back. Nothing in this market moves in a straight line, especially when positioning is crowded and the broader AI complex is still wrestling with capex fatigue, valuation nerves and the question of whether hyperscalers can keep spending at this pace forever. But fading Micron after this report is no longer simply a valuation call. It is a wager that a global memory shortage, multi-year customer commitments and an AI infrastructure arms race are all about to cool at the same time.

What a knee-jerk!!

The summer market may still want to sell strength. But Micron has just reminded traders that some rallies are not driven by hot air. Some are driven by contracts, capacity constraints, and customers willing to put real money down to make sure they are not left standing outside the AI factory when the doors close.

On a side note, it’s time for me to prepare for the Tartan Army Bhoys as they take on Brazil in the World Cup !!!

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.