The AI infrastructure trade is moving from a capex-acceleration to a capex-digestion regime, in contrast to the prior 18 months where uncapped enterprise token consumption underwrote every upward revision.

- AI adoption in enterprise is usage-based, agentic, recursive, and easy to overconsume. Uber burned its entire 2026 AI coding budget in four months; Microsoft is cancelling internal Claude Code licenses by June 30.

- Hyperscaler capex is the foundation of the AI infrastructure trade. The Big Four (Microsoft, Alphabet, Meta, Amazon) will spend roughly 94% of operating cash flow on capex in 2026 versus a 10-year average of 40%. This spending flows downstream into Nvidia, AMD, the memory and networking complex, power, cooling, etc.

- The AI infrastructure investment thesis rests on an assumption: that aggregate token consumption will scale near-vertically through the decade, justifying the hyperscaler capital plans that supply the compute.

- Enterprise AI adoption follows a J-curve: pilot period, digestion pause, production reacceleration. A near-term slowdown in token consumption is a likely scenario. Equity prices will respond sharply, creating a window for correction within an intact long-term trend.

The First Wave of Enterprise AI Cost Discipline

Uber (NYSE:) deployed an agentic coding assistant to roughly 5,000 engineers in late 2025 and exhausted its full-year 2026 AI tooling budget within four months. Heavy users consumed $500–$2,000 per engineer per month in API charges. Uber’s leadership has publicly acknowledged that token consumption growth is not tracking to measurable consumer-product output. Uber is not alone in reassessing its approach to AI usage. At Duolingo, management reversed course on a policy that had tied employee performance evaluations to AI usage, after staff raised concerns that the metric rewarded tool adoption rather than actual results.

is following a similar path. The company is winding down internal Claude Code access across its Experiences + Devices group, the engineers building Windows, Microsoft 365, Outlook, Teams, and Surface — by the end of its fiscal year. The framing is toolchain unification; the binding constraint is per-token cost on agentic workloads at headcount scale.

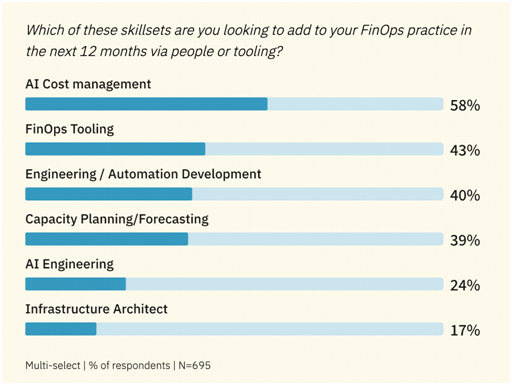

The State of FinOps 2026 Report shows the share of organizations actively managing AI spend doubled from 31% (2024) to 63% (2025), and has now hit 98% in 2026. AI cost management has moved from “emerging” to core FinOps scope faster than any prior category.

Source: https://data.finops.org/

AI Cost Behavior Breaks the SaaS Playbook

The Uber and Microsoft cases reflect a cost model that enterprise finance functions have not previously had to underwrite. SaaS pricing is seat-based and forecastable: a known headcount produces a known annual expense. AI inference is different, it is usage-based rather than seat-based, agentic rather than user-initiated, recursive rather than linear, and easy to overconsume.

A single agent task can call the underlying model multiple times, spawn subtasks that call the model again, query files, invoke external tools, and generate large context windows that re-bill on every turn.

Why This Matters for the AI Infrastructure Trade

The AI infrastructure investment thesis rests on an underwriting assumption: that aggregate token consumption will scale near-vertically through the decade, justifying the hyperscaler capital plans that supply the compute.

The hyperscalers are the primary middlemen delivering compute in the AI boom, all their recent qualitative and quantitative commentary told the same story: demand far exceeds supply, and justify their increase in CapEx.

Their 2026 capex of approximately $700B is justified by the projection that inference workloads will multiply by orders of magnitude as agentic AI moves from pilot to production.

The projected demand curve was itself extrapolated from current usage, when many enterprises ran with effectively uncapped consumption. Those pilots produced the token-growth slope that flows into hyperscaler capacity planning, into ’s data-center revenue forecasts, and into the forward earnings models for the entire AI supply chain, power, cooling, networking, memory, custom silicon.

Source: https://www.generativevalue.com/p/the-hyperscalers-and-the-compute

Enterprise AI Adoption J-Curve

Token volume is not the same as economic demand. If enterprise pilots were run with weak budget discipline, experimental workflows, and little regard for inference cost, then early token growth can overstate normalized production demand.

Enterprise AI adoption is very possibly a three-phase J-curve rather than a linear ramp.

Phase 1 — Pilot (2025–now). Enterprises experiment aggressively. Token usage grows quickly because access is relatively unconstrained, use cases are broad, and internal controls are immature. This is the phase that produced the early demand signal hyperscalers, Nvidia, and the AI supply chain extrapolated forward into capacity plans. It is also the phase that produced the cost surprises now triggering procurement discipline.

Phase 2 — Enterprise digestion (2026–2027). Token growth slows. Companies discover that workflows must be rewired, data cleaned, permissions managed, employees trained, budgets set, and model routing decided between frontier and cheaper alternatives. From the outside, this phase looks like demand weakness.

Phase 3 — Production reacceleration (2027 onward). Once workflows are redesigned, token usage can surge again on a higher-quality base. AI consumption shifts from discretionary human prompting to embedded workflows.

The market is unlikely to wait for the three phases to resolve. Equity prices respond to the slowdown signal before the cause is verifiable, which creates a window for correction within an intact long-term trend.

Bottom Line

Enterprise AI is entering a digestion phase. Token growth will slow as workflows are redesigned and spend is rationalized; this is more probably the J-curve transition than terminal demand weakness.

The market is likely to misread the slowdown. A correction in AI infrastructure equities is probable even if the long-term thesis remains intact.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.