The Argument No One Is Making Loudly

Sixteen consecutive years of positive sales growth is not an accident. It is not a function of a particularly benign cycle, a one-time acquisition, or a favorable macro that lifted every boat. It is what happens when a business owns a critical chokepoint in a $44 billion market, operates from a branch network that took decades to build, and serves an end customer whose underground pipes wear out on a schedule that does not adjust to interest rates.

Core & Main Inc () distributes pipes, valves, fittings, meters, storm drainage components, and fire protection products to the municipalities, private water companies, and contractors who build and maintain the water infrastructure beneath American cities. The company sits at the most defensible position in that supply chain: between 5,000 suppliers who lack the scale to reach 60,000 fragmented local customers, and those customers who lack the purchasing power and logistics infrastructure to go direct. That intermediary position, secured by 370 locations and relationships built over decades, is what has kept revenues growing through recessions, rate cycles, pandemic supply disruptions, and a softening residential market in fiscal 2025.

The market has not been generous to this. The stock trades at approximately $50 per share, putting it at roughly 12.5 times trailing adjusted EBITDA. For a company with a 19% share of a $44 billion domestic market, growing through a combination of organic gains and disciplined acquisition, that multiple prices the business as though the compounding opportunity is modest. The American Society of Civil Engineers grades the country’s drinking water infrastructure a C minus and estimates $625 billion is needed over the next two decades to address it. The $55 billion allocated under the Infrastructure Investment and Jobs Act, the first sustained federal commitment to this sector in modern history, was still flowing through state revolving fund programs into local projects as of early 2026. The investment need is structural, not cyclical. Core & Main is the distribution infrastructure through which a meaningful share of it will flow.

The Branch Network and What It Takes to Build One

A municipality in need of twelve-inch ductile iron pipe fittings for an emergency repair at six in the morning does not compare prices online and wait three days for delivery. It calls the Core & Main branch in the adjacent zip code, which stocks those fittings, knows the contractor arriving to collect them by name, and can extend the credit terms municipal procurement requires. That relationship has often existed for years. It cannot be replicated by a new entrant with capital and ambition. It requires a branch, trained people, calibrated inventory, and time.

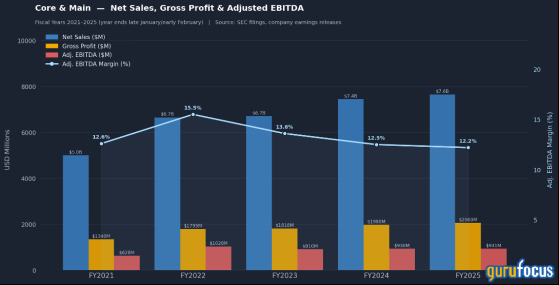

More than 370 branches in the United States and Canada serve as the distribution infrastructure that makes this possible at scale. Each branch carries inventory calibrated to its local market. Each employs people with technical product knowledge specific to that market’s dominant product mix, whether that is fusible high-density polyethylene pipe in regions with aggressive soil conditions, advanced metering infrastructure in municipalities mid-replacement cycle, or fire protection fabrication services in high-density commercial corridors. The economics of the branch model are not glamorous. Gross margins run approximately 26 to 27%, earned through purchasing scale, private label expansion, and pricing discipline. Adjusted EBITDA margins have normalized to 12.2% in fiscal 2025 from the 15.5% peak of fiscal 2022, which reflected the extraordinary pricing environment of the post-pandemic supply disruption. That 12.2% is management’s stated floor, and the private label and sourcing initiatives underway are intended to deliver incremental margin improvement from that base rather than defend against further compression.

The branch network is simultaneously the competitive moat and the acquisition platform. When a regional waterworks distributor in an underserved geography comes to market, Core & Main acquires it, integrates it into its purchasing and logistics infrastructure, and expands margins immediately through the scale advantages the parent provides. Fiscal 2025 saw two acquisitions: Canada Waterworks, extending the platform into the Canadian market for the first time, and Pioneer Supply in Oklahoma and Texas, adding five branches in priority growth markets. These deals were small in the context of a $7.65 billion revenue base but follow a pattern consistent for fifteen years. Ten new greenfield branches were also opened during and shortly after fiscal 2025 in markets management identified as having above-average demand profiles. The acquisition machine is not built on hope. It is built on a functioning integration capability, an established pipeline, and the local knowledge to identify where the network has genuine gaps.

is the only other competitor at national scale. Everything else in the $44 billion addressable market is regional, local, or product-specific. That duopoly, combined with the branch density that both companies have spent years accumulating, creates a structural barrier that capital alone cannot quickly cross. The relationships, the inventory intelligence, and the contractor trust that a well-run branch accumulates over a decade of operation represent a genuine and durable competitive advantage that the current valuation does not fully price.

Three End Markets and the One That Is Changing

Municipal demand, which accounts for roughly 42% of net sales, is driven by the non-discretionary need to repair and replace aging underground infrastructure. Pipes installed in the 1950s and 1960s do not care about interest rates or budget cycles. They fail, and the municipality must replace them, whether or not the federal procurement environment is favorable. Non-residential construction, representing approximately 39% of net sales, is tied to commercial and industrial build activity but carries specific technical product categories, particularly treatment plant solutions and fusible HDPE pipe, where Core & Main’s project management capability and product expertise create pricing power that commodity pipe suppliers cannot match. Residential, the smallest end market at roughly 19% of net sales, is the most cyclical and was the source of the volume softness that pressured the second half of fiscal 2025.

That last point deserves more weight than the municipal framing typically allows it. Non-residential and residential together represent roughly 58% of total revenue, and both segments follow project activity in ways that emergency pipe replacement does not. A commercial contractor on an industrial or office development compares suppliers, negotiates pricing, and defers orders when project economics shift. A residential developer responds to lot development margins and permitting timelines. In a material construction downturn, volume across these two segments declines simultaneously, pricing competition increases, and the project backlog thins. The comparison that is tempting to reach for, a utility-like business collecting fees on non-deferrable spend, does not hold for a business where the majority of revenue is project-driven. Core & Main is more resilient than a typical industrial distributor because of the municipal anchor and the product necessity. It is not a utility.

The meter category is where the long-term story is changing. Meter products grew 31.8% year-on-year in fiscal 2024 to $692 million, the fastest growth of any major product line in the portfolio and approximately 9% of net sales at the time. That is the most recently disclosed full-year annual breakdown; throughout fiscal 2025, management consistently described meter sales as outpacing core market growth with growing backlogs and strong shipments, though the pace of a 31% annual expansion is unlikely to repeat in every year ahead. The structural driver is genuine: municipalities replacing manual-read systems with advanced metering infrastructure gain real-time consumption monitoring, remote leak detection, and elimination of physical meter read labor, and the economics of inaction become harder to justify as federal funding flows through state revolving programs into local projects.

The commercial model around meters is different from the rest of Core & Main’s product portfolio. The company offers multi-stage smart metering solutions that include meter accessories, network infrastructure, software installation, training, and long-term service contracts. A municipality that purchases meters through Core & Main, has Core & Main coordinate the installation, and signs a service agreement for ongoing network management creates a multi-year revenue relationship from what would otherwise have been a one-time equipment sale. That evolution toward contracted recurring revenue in a product category tied to essential public infrastructure is a genuine change to the quality of the earnings base. It is also accurate to note that a portion of meter demand is linked to new construction and infrastructure upgrade cycles rather than purely non-discretionary replacement; in a broad demand contraction, this category is not entirely insulated from project delays.

The Cash the Business Produces and What It Does With It

Core & Main generated $650 million of operating cash flow in fiscal 2025, a 70% conversion ratio against $931 million of adjusted EBITDA. Free cash flow after $46 million of capital expenditures was $604 million. Distribution businesses release working capital as volumes fall: receivables shrink and inventory investment declines, providing cash precisely when balance sheet flexibility matters most. Core & Main demonstrated this in fiscal 2025’s second half, when softening residential demand produced the working capital release that supported $329 million of net debt reduction and $155 million of share repurchases simultaneously. The same mechanics apply in reverse as volumes recover. Rebuilding inventory and extending credit to a growing customer base consumes cash during an upcycle at roughly the same rate it was released in the downturn. Working capital is a timing benefit in a contraction. It does not create value across a full cycle.

Net debt at $1.95 billion and 2.1 times adjusted EBITDA falls within management’s stated target range of 1.5 to 3.0 times and is declining. The senior term loan structure, divided between a facility due 2028 and a facility due 2031, provides funding certainty through the demand normalization period. Fiscal 2026 guidance of $950 to $980 million in adjusted EBITDA against a flat pricing and end-market performance assumption means that any recovery in residential demand, any acceleration of IIJA disbursements, or any contribution from recent acquisitions above base case would improve both the absolute cash generation and the leverage trajectory.

The share count is shrinking. Approximately 3.2 million Class A shares were repurchased during fiscal 2025 at an average price near $48, with an additional 800,000 shares bought after year-end. More than $600 million remained authorized at the time of the March 2026 earnings call. For a business with a cost of equity implying returns well above its weighted average cost of capital at current prices, the arithmetic of repurchases is favorable regardless of the near-term demand environment. Adjusted diluted EPS grew 7% to $2.97 in fiscal 2025. The combination of modestly growing earnings and a declining denominator creates a per-share compounding dynamic that the market currently prices at roughly 16.8 times.

Who Holds This and What the Positions Suggest

D1 Capital Partners, Daniel Sundheim’s firm, holds 2.6 million shares at approximately $138 million. The 48.85% trim of roughly 2.5 million shares in the most recent period is a significant reduction that deserves honest acknowledgment. A fund with D1’s orientation does not hold 2.6 million shares of a waterworks distributor without a specific view. The residual position, held through the trim at an average buy price of $50.45, suggests the reduction reflects portfolio-level risk management rather than a fundamental reassessment. The remaining position at the same approximate average cost basis is still a meaningful expression of conviction.

Samlyn Capital holds 2.8 million shares at $148 million and increased its position 6.8% in the most recent period with approximately 181,000 additional shares against an average buy price of $31.77. Fresh capital added at prices roughly 58% above the historical cost basis is not a passive holder maintaining a position. It is a manager extending a position at materially higher prices, which requires a specific updated view on the forward return at current levels.

Soros Fund Management and Tudor Investment Corp both opened entirely new positions in the same quarter, each acquiring shares at an average price near $52.90. Two new positions at nearly identical entry prices in the same reporting period is not coincidental. Both managers tend toward situations where the risk-reward profile implied by the current price is wider than the market appears to recognize.

DE Shaw more than doubled its position, adding approximately 1.6 million shares for a total of 2.5 million at an average price of $53.29. A position increase of that magnitude from a quantitative firm suggests the stock sits at an intersection of factor characteristics, improving profitability, declining leverage, earnings per share acceleration, and a valuation gap, that the systematic model has flagged as mispriced.

ACK Asset Management holds 900,000 shares representing 5.91% of its entire portfolio with no reported change in the most recent period. The average buy price of $57.09 is above where the stock currently trades. A full position held at a mark-to-market loss through a period of guidance reductions and end-market softness is evidence of a manager who has done the work and arrived at a different conclusion than the price reflects. The absence of reduction is its own form of statement.

What the Current Price Actually Prices

At approximately $50 per share with roughly 195 million shares outstanding, Core & Main’s market capitalization is approximately $9.7 billion. Adding net debt of $1.95 billion produces an enterprise value of approximately $11.65 billion, against trailing adjusted EBITDA of $931 million, which implies 12.5 times. Against the fiscal 2025 free cash flow of $604 million, the EV/FCF multiple is approximately 19.3 times. Ferguson Enterprises, the only direct national competitor, trades at 16.1 times EBITDA with a 14.5% ROIC. distributes storm drainage products, overlaps substantially with Core & Main’s customer base, and trades at 12.4 times trailing EBITDA on a net-cash balance sheet with a 22.2% ROIC that reflects the margin advantages of manufacturing relative to pure distribution. , the landscape distribution analog and a proxy for specialty distributor multiples in adjacent categories, commands 17.2 times EBITDA.

The Ferguson comparison is the most direct. One national waterworks distributor trades at 16 times EBITDA. Its only national competitor trades at 12.5 times. The ROIC differential, which currently favors Ferguson at 14.5% versus Core & Main at approximately 11%, reflects the historical leverage from the Clayton, Dubilier acquisition rather than a permanent quality gap. As debt declines toward management’s target, that differential narrows.

An owner underwriting Core & Main at today’s price is starting from a free cash flow yield of approximately 5.2% on enterprise value, with a buyback program actively reducing the share count and a management team guiding to $950 to $980 million of adjusted EBITDA in fiscal 2026. A stable multiple at 12.5 times on the midpoint $965 million produces an enterprise value of $12.1 billion and an equity value near $52 per share, a modest premium to today’s price without any re-rating. A migration toward Ferguson’s 16 times multiple on the same earnings base produces an equity value near $65 per share, a 30% return. The opportunity cost of not owning this business is the opportunity cost of not owning the infrastructure distribution layer through which a structurally underfunded sector will direct hundreds of billions of dollars over the next decade.

The downside requires honest framing, and the context around it matters. Core & Main has been a public company since 2021 and operated in its current form as a private equity asset from 2017; it has not traded through a full construction cycle in its present structure. The fiscal 2022 revenue expansion and the 15.5% EBITDA margin peak of that year were substantially driven by product price inflation during the post-pandemic supply disruption rather than purely organic share gains. That tailwind has reversed, and the current 12.2% margin reflects its absence. A broad construction downturn, one that contracts non-residential project starts and residential lot development simultaneously, would put pressure on roughly 58% of revenue at once. Working capital would release cash as volumes fell, but rebuilding inventory and customer credit when the cycle turned would consume that same cash in the recovery. The senior term loans mature in 2028 and 2031, creating no near-term refinancing pressure; if interest rates were to rise during a demand contraction rather than fall alongside it, the variable-rate exposure would compound operating pressure in a way that a fixed-rate structure would not.

At 2.1 times net leverage, the balance sheet is not fragile. But an owner entering at 12.5 times EBITDA should do so understanding what this business is: a well-run distribution operation with genuine structural advantages and real cyclical exposure across a majority of its revenue, a limited clean public history in its current form, and a balance sheet still normalizing from a decade of consolidation. Whether the Ferguson premium is achievable depends on whether the ROIC recovery and the meter transition deliver enough evidence over the next twelve to eighteen months to close a 3.5-turn gap that may partly reflect structural differences rather than temporary distortions.

Final Thought

The business that distributes the pipes, valves, meters, and fittings through which American water infrastructure is built and maintained does not generate headlines. It does not have a data center angle, a defense contract, or a software platform. It has branches, relationships, and a customer base that replaces what corrodes. That is not a less interesting business. It is a more durable one.

Core & Main has compounded through recessions, rate cycles, and two distinct housing downturns by being the reliable, technically capable, locally present distribution partner that municipalities and contractors cannot easily replace. The meter business is changing the quality of the revenue base in ways that a pure distribution multiple does not fully capture. The balance sheet is improving on schedule, not dramatically, but consistently.

For a long-term owner, the combination of a structural market position, a recovering earnings trajectory, a balance sheet generating more cash than the business requires to operate, and a persistent valuation discount to the only directly comparable company at the national scale is a more compelling starting point than current prices suggest. The infrastructure beneath American cities wears out. Core & Main will sell much of what is needed to replace it. The 16th consecutive year of positive sales growth will not be the last.

This content was originally published on Gurufocus.com

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.