Listen to the audio version of this article (generated by AI).

Tom Yeung here with your Sunday Digest.

“Everyone knows” may be one of the most dangerous terms in investing:

- “Everyone knows internet stocks don’t need profits”…

- “Everyone knows real estate prices only go up”…

- “Everyone knows Bitcoin will hit $1 million”…

That’s because “everyone knows” means every investor collectively believes the same thing. Once that happens, there’s no one left on the opposite side of a trade.

And there’s the problem. If there are only buyers and no sellers, you end up with speculative bubbles from Las Vegas real estate to meme coins that can end in disaster.

A new “everyone knows” phenomenon is now gripping markets: that the U.S. Federal Reserve will not cut rates in 2026. In fact, The Wall Street Journal reported last week that regional bank presidents are starting to talk about potentially hiking rates.

That’s driven investors into companies that do well when rates are high, namely cash-rich behemoths like Apple Inc. (AAPL) and Alphabet Inc. (GOOGL). These titans can fund their own growth without worrying about borrowing cash. In fact, the Magnificent Seven stocks now make up roughly 35% of the entire S&P 500, up from around 20% in early 2023.

But what about the other side of that trade – those betting that rate cuts could still be on the table?

InvestorPlace Senior Analyst Louis Navellier is one of them.

He rightly senses that the jobs market and American consumption are weaker than Wall Street believes. The Fed might be forced to reduce rates even as gasoline-led inflation persists.

To capitalize on this trend, Louis has identified 53 small-cap stocks he calls his “Exclusion List” — companies that are simply too small for major Wall Street firms to buy aggressively.

These are mostly high-growth companies that need cheap cash to fund further expansion… and he’s sharing this list free with folks who sign up to attend his May 13 presentation. During the presentation, Louis will highlight the stocks he believes have the highest conviction on that list.

To give you a sense of these 53 companies, I’ve chosen three to share with you today.

Let’s dive in…

Small-Cap Stock to Buy No. 1: Watt Goes Up

Rising global energy prices have put solar power back on the menu.

Solar farms are quick to build, unaffected by high fossil fuel prices, and still benefit from federal programs like the Inflation Reduction Act (IRA) that aren’t due to expire for many more years. In fact, the U.S. Energy Information Administration expects that solar will make up 51% of all new electric generating capacity in 2026, led by states like Texas and Arizona.

Many of solar’s “big boys” have already seen their stock prices shoot up. Hanwha Solutions Corp., a South Korean behemoth with a major solar division, has seen shares rise 420% since 2025.

But the rush into mega-cap solar makers has left smaller players by the wayside. That brings us to our first small-cap candidate:

TOYO Co. Ltd. (TOYO).

TOYO is a vertically integrated solar manufacturer headquartered in Tokyo and listed on the Nasdaq. The company produces next-generation TOPCon (tunnel oxide passivated contact) cells, which deliver higher solar conversion rates than the older PERC standard that dominates installed capacity.

The firm recently became the largest non-FEOC (foreign entity of concern) maker of these TOPCon cells after opening a 4 gigawatt cell factory in Ethiopia and acquiring a 1GW facility in Houston last year, which they plan to double in size. This designation matters because projects claiming IRA manufacturing tax credits must prove their supply chains are free of FEOC content. That gives TOYO an immense advantage over Chinese rivals like JinkoSolar Holding Co. Ltd. (JKS).

That’s helped TOYO reach a growth inflection point. Revenues are expected to surge 95% to $832 million this year, and then rise another 33% in 2027 as U.S. manufacturing expands. Profits should rise even faster as the company reaches scale.

Best of all, shares are remarkably cheap – and even more so if rates fall. Shares trade for below 5X forward earnings, demonstrating how many small-cap companies are mispriced simply because Wall Street doesn’t know they exist.

Of course, investors should be aware of the risks in small-cap stocks, especially with a tightly held firm like TOYO. The company’s holding structure is opaque, and its balance sheet involves related-party vendor financing that looks to me like a house of cards. It’s a bit like Tesla Inc. (TSLA) in 2008 or 2017, where a firm makes a massive financial leap without any guarantee of landing on solid ground… all while “window dressing” their financial reports to calm investors. The stock could go to zero, especially if rates go up and financing evaporates.

If TOYO’s bets pay off, however, the stock is worth multiples of what it is today. And according to Louis’ system, it’s a wager that could well pay off.

Small-Cap Stock to Buy No. 2: Floating Along

The Strait of Hormuz closure has been a disaster for global oil logistics. Roughly 1,600 ships are stuck in the Persian Gulf, including at least 50 massive carriers and hundreds of smaller tankers.

A reopening of the Strait won’t bring normalcy for months. Shipping companies will hesitate to send new ships through the chokepoint – wary of hitting sea mines or trapping more of their fleet if the shooting resumes. Besides, damage to the Gulf’s oil terminals is so extensive that it could take until 2027 to get production back up to speed.

However, that’s proven to be a near-bonanza for shipping companies. They have seen charter rates spike as remaining ships are forced to make longer voyages. Every extra day at sea worsens the shortage because ships are not available for new charters.

That should benefit one of Louis’ small-cap tankers on his 53-stock Exclusion List:

Ardmore Shipping Corp. (ASC).

Ardmore is a Bermuda-based shipping company specializing in transporting refined petroleum products. The firm owns 25 vessels (plus one chartered ship) and has a long history of positive cash flows. They have generated cash in 13 of the past 15 years.

The recent spike in shipping rates will now create windfall profits for Ardmore. Analysts expect net income to rise 25% on average over the next two years, and this figure could be even higher if shipping rates remain this elevated. Below is the graph of the Baltic Clean Tanker Index – the most relevant one to Ardmore’s fleet. As you can see, charter rates have risen 3X since last year.

The Baltic Clean Tanker Index

Source: L/S/E/G

Ardmore also stands to gain financially from lower American interest rates. Twenty of the company’s ships are mortgaged based on the Treasury’s secured overnight financing rate (SOFR), so lower rates instantly mean less interest payments. It will also decrease the cost of buying new ships.

Fortunately, Wall Street hasn’t quite caught up yet.

Shares of the shipping firm trade at just 12.5X forward earnings and 9.3X cash flows – within striking distance of long-term averages. The stock is also supported by a roughly $21-per-share of net asset value, using the company’s recent $35.5 million sale of an older vessel as a guide. (That means the company could theoretically sell its entire fleet, pay off debt, and still have roughly $21 per share in cash left over for shareholders).

With the stock trading under $19 today, that seems a deal worth taking.

Small-Cap Stock to Buy No. 3: The Moonshot Biotech

The biotech industry is notoriously reliant on financing. New drugs can take years and billions of dollars to develop before they ever reach the commercial stage — making biotech one of the most interest-rate-sensitive corners of the market.

Falling rates could present a real opportunity here. Not only do discount rates drop (making future cash flows more valuable today), but cash-hungry firms can borrow more cheaply to fund the growth they need.

That brings us to our third pick:

Nautilus Biotechnology Inc. (NAUT).

Nautilus is a pre-revenue startup building what could become the standard platform for protein analysis. Management expects a commercial launch by late 2026, with installations beginning in early 2027.

Here’s why that matters. Today’s standard approach — called mass spectrometry — requires researchers to chop proteins into fragments, and then try to reconstruct what they had. It’s slow, labor intensive, and prone to error with proteins it hasn’t seen before.

Nautilus’s system works differently: It analyzes proteins intact, using fluorescent probes to map their structure without breaking anything apart. Think of it as reading a book rather than shredding it and guessing the plot from the scraps.

The practical upside is significant. Diseases like Alzheimer’s, Parkinson’s, and ALS involve subtle protein variations that current tools routinely miss. A better map means better drug development — and potentially faster answers to questions researchers have been stuck on for decades.

The company is on track. A successful prototype was revealed in February 2026, and respected institutions like the Buck Institute are already testing the machines. Insiders have been buying — five purchases over the past year, including one as recently as March. That’s one of my favorite “Buy” signals in the biotech world.

If rates fall and Nautilus hits its timeline, this is the kind of stock that can move dramatically. If they don’t, it carries real risk. But according to Louis’s system, the risk-reward here is worth taking seriously.

Don’t Rule Out Rate Cuts Quite Yet

Most people on Wall Street have given up hope for rate cuts this year.

If March inflation jumped to 3.3% on high gas prices, surely the Fed must step in with higher rates?

Betting markets have moved in the same direction. More than half of bettors now predict zero cuts this year.

Still, December 2026 is a long way from now, and plenty can happen in seven months. In fact, we could see a downturn… or even a recession.

On Thursday, Whirlpool Corp. (WHR) warned that the U.S.-Iran conflict had caused a “recession-level industry decline.” In prepared earnings call remarks, the appliance maker’s CEO said he no longer anticipates a full recovery in 2026. This comes days after the CEO of The Kraft Heinz Co. (KHC) said that customers are “literally running out of money at the end of the month.”

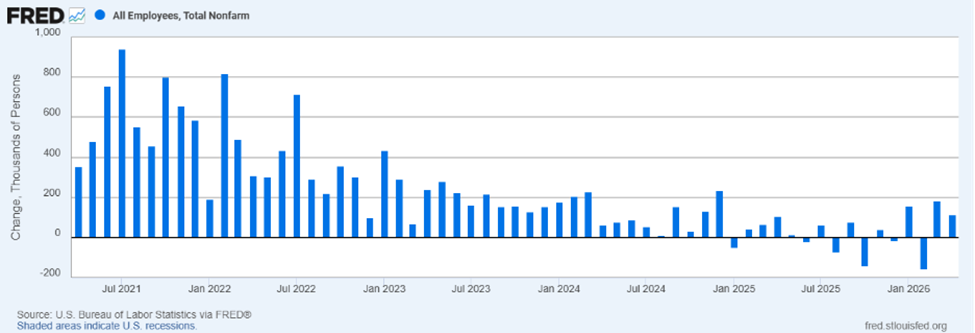

Friday’s “solid” jobs report numbers are also weaker than they seem. The chart below shows how employment additions have actually looked in broader historical context.

Monthly non-farm U.S. jobs added

Source: St. Louis Federal Reserve

That’s why it’s crucial you tune in to Louis Navellier’s special broadcast on May 13, at 1 p.m. Eastern. During that free event, he’ll outline why he still believes rate cuts are on the table, and why small-cap stocks are some of the best places to invest right now.

In addition, Louis will discuss the rest of his 53 small-cap “Exclusion List” picks and reveal the one stock – name and ticker – he believes is especially well positioned for the next phase of the market.

Sign up for the May 13 broadcast here.

Until next week,

Thomas Yeung, CFA

Market Analyst, InvestorPlace

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.