’s stock price hit bottom earlier this year and is on track to reverse. While persistent issues like cash burn remain, the company appears to be gaining traction and has a significant acquisition ahead.

The Acquisition

LivePerson is a conversational cloud AI platform whose business is driven by a messaging platform, enabling brands to converse with consumers across channels.

The benefits of SoundHound’s acquisition of LivePerson are substantial, including expanded reach, enhanced services, cost-saving opportunities, technological advancements, and accelerated growth. LivePerson’s portfolio includes hundreds of top-tier global brands, including airlines and financial institutions, thereby expanding its reach and cross-sell opportunities.

If the acquisition closes as expected, the merged company will provide a unified voice and digital messaging across the communications ecosystem. The combination is expected to accelerate and sustain growth, as their polled data will enhance AI training and improve accuracy.

Path to Profitability

Ultimately, the combination is expected to accelerate sustainable growth while improving the path to profitability. As it stands, the outlook for profits is mixed. Company execs are forecasting an inflection in profits by early 2027, while many analysts don’t expect sustainable profitability until 2028. The takeaway for investors is that ample uncertainty remains, but the risk is to the upside, given the ultra-low stock price, the recent acquisition of Amelia, and the launch of the firm’s OASYS product.

Amelia enables voice-activated, automed customer service and employee-facing interactions, including agentic AI capabilities. It expanded SoundHound’s services beyond simple customer interactions, delivering enterprise-quality agentic capabilities. OASYS is a self-learning, agentic AI platform that enables quick, easy agentic AI development, deployment, and upgrading. Its key aspect is the self-learning capability, enabling the system to learn from new data, build AI and improve agentic operations over time.

Mixed Quarterly Results Send SoundHound Lower

SoundHound had a decent Q1 despite the mixed bottom-line result and the market reaction. The company reported $44.2 million in net revenue, up nearly 52% year-over-year (YOY) and 375 basis points (bps) better than expected. The strength was driven by all verticals and categories, with noteworthy strength in the core business. Automotive and Internet of Things (IoT) grew by nearly 90%, adjusted for acquisitions, underscoring the business model strength. New customers are becoming long-lasting customers, increasing their service use.

Margin was a mixed bag, with the adjusted gross margin strong at 49.7% and adjusted EBITDA in the red. However, non-recurring one-offs related to the growth strategy are to blame, and guidance is more robust. The company reaffirmed its revenue target, expecting $242.5 million at the midpoint, above analyst consensus, forecasting robust growth for the remainder of the year.

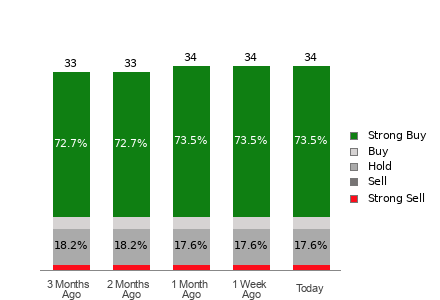

Cautious Analysts Forecast 50% Upside: Institutions Buy Into the Outlook

The analyst response following the release aligned with 2026 analyst activity, showing caution amid continued losses but optimism about the future. The 10 tracked by MarketBeat carry a consensus Moderate Buy rating, with a 60% Buy-side bias, and more than 70% upside at the consensus target. Assuming traction is evident in the coming quarters, specifically regarding the LivePerson acquisition and/or the path to profitability, sentiment will likely firm, strengthening the catalyst.

Institutions are buying into the outlook, regardless of near-term headwinds. MarketBeat data reveals the group owning only 20% of the stock but accumulating at a robust, approximately $3-to-$1 pace over the trailing 12 months. Activity was strong in Q1 2026, the trend extended into early Q2, and will likely remain positive as the year progresses.

The biggest risk is that SoundHound fails to execute its strategy, including the acquisition of LivePerson, in which case the stock price downside may be unlimited.

Short Selles a Risk and Opportunity in SoundHound Stock

Short-sellers are leaning hard into the SoundHound trade. Activity has ramped over the past two years, driving short-interest to approximately 40% of the stock, creating a robust headwind for market action. With this in place, upside in the stock price is limited, but a catalyst for short-covering is in the works.

LivePerson acquisition aside, SoundHound is well-positioned to gain traction in the current and upcoming quarters; add in a LivePerson acquisition, and the short-covering can easily become a squeeze. In this scenario, SOUN price action can easily revert to the analysts’ consensus target, near the mid-point of the long-term trading range.

The technical action is bullish, suggesting that short-covering is already underway. The market is forming a Head & Shoulders pattern, setting up to confirm the second shoulder with the post-release price dip. The likely outcome is that support near $8 is confirmed, and a rebound quickly follows.

The technical action is bullish, suggesting that short-covering is already underway. The market is forming a Head & Shoulders pattern, setting up to confirm the second shoulder with the post-release price dip. The likely outcome is that support near $8 is confirmed, and a rebound quickly follows.

The critical resistance point is the pattern’s neckline, which indicates a bullish bias. A move above $9.75/$10 may be the technical trigger to accelerate short covering.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.