Despite a $160 billion market cap and a 556% return over the last decade, may still fly under the radar for many investors. That said, shares are down about 25% from their highs and have fallen almost 15% over the past year.

The company develops technologies that help physicians perform minimally invasive procedures worldwide. Its key products include the da Vinci Surgical System for complex surgeries and the Ion endoluminal system for lung biopsies. The company also provides instruments, training, services, and digital tools to support robotic surgery programs.

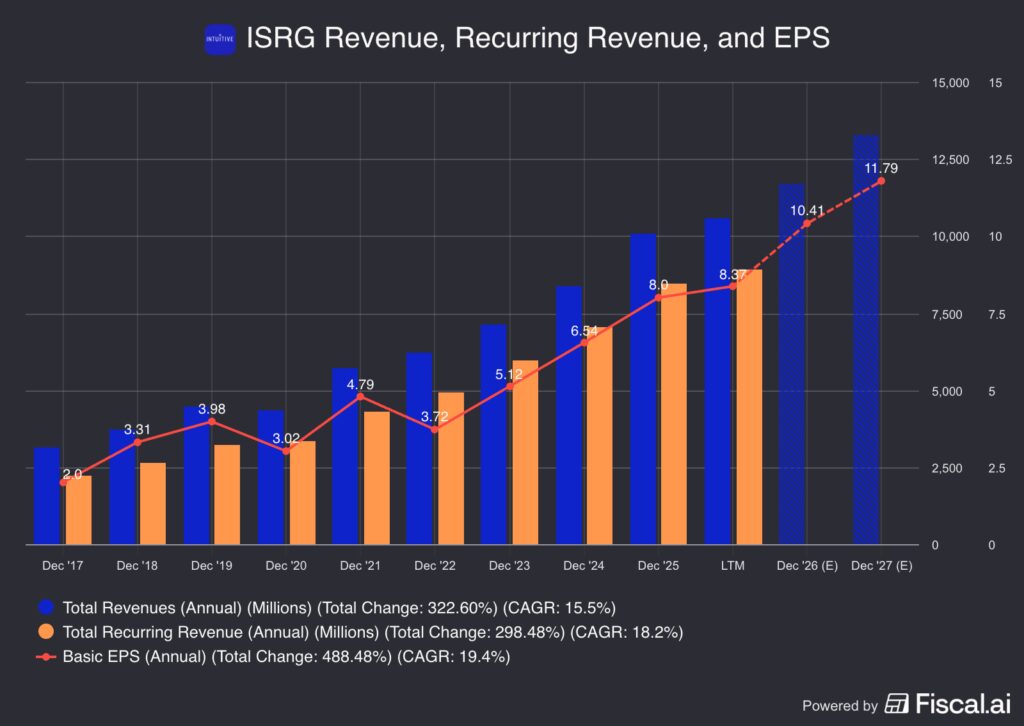

For years, Intuitive Surgical has been a steady operator within the healthcare space. Like many others though, it saw some lumpiness in its business from 2020 to 2022. Since then, it’s been relatively smooth sailing for earnings, revenue, and recurring revenue:

Future Growth Projections

Looking ahead, analysts expect pretty consistent results of Intuitive Surgical, with expected annual earnings and revenue growth in the 13% and 16% range. According to Bloomberg, analysts project the following:

- Earnings Growth: 15.8% in 2026, 13.6% in 2027, and 13.8% in 2028

- Revenue Growth: 16.4% in 2026, 13.2% in 2027, and 13.1% in 2028

Analysts currently have a consensus price target of ~$576 on ISRG stock, implying about 27% upside to today’s stock price.

Diving Deeper — Valuation

Mid-teen growth rates are very solid and represent steady expansion. However, there may be some hesitancy from investors to pay up for ISRG stock for growth that’s strong, but not necessarily out of this world. That’s where valuation-focused investors may get hung up on Intuitive Surgical.

On the one hand, ISRG is trading at its lowest forward price-to-earnings ratio in almost three years (white line). However, it’s still above the valuation zone of 38x or lower, which has marked a trough since 2019. On a forward price-to-FCF basis (blue line), the stock is near a trough zone of roughly 33x. At the end of the day though, some might still argue that this valuation is too much for mid-teen growt Source: Bloomberg, eToro. 5/7/2026

Source: Bloomberg, eToro. 5/7/2026

Risks

Key risks for Intuitive Surgical include its heavy reliance on da Vinci procedure growth, which can be pressured by hospital staffing issues, elective-surgery trends, and tighter hospital budgets. The company also faces execution risk around the da Vinci 5 upgrade cycle, rising competition in surgical robotics, tariff and margin pressures, and China-specific risks tied to pricing, reimbursement, quotas, and local competitors. Meanwhile, slower adoption of newer platforms like Ion, potential regulatory or safety issues, and ISRG’s premium valuation leave little room for disappointment.

The Bottom Line

Intuitive Surgical has become a blue-chip stock within the medical device industry. However, shares have struggled less because the business is broken and more because the stock was priced for perfection. Expectations were sky-high, margins have been under scrutiny, and investors are questioning whether growth can keep justifying the premium multiple.

As the stock price has come down, investors are now questioning whether a long-term opportunity is in front of them or if it’s a red caution flag to stay away.

***

Disclaimer: Please note that due to market volatility, some of the prices may have already been reached and scenarios played out. Content, research, tools, and stock symbols displayed are for educational purposes only and do not imply a recommendation or solicitation to engage in any specific investment strategy. All investments involve risk, losses may exceed the amount of principal invested, and past performance does not guarantee future results.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.