Takeaways

- Equities are no longer broadly based; the entire tape is being driven by one force, AI spend, with everything else orbiting that single gravity well

- Hyperscaler capex is the fuel line, as long as Microsoft, Amazon, Alphabet and Meta Platforms keep spending aggressively, the AI flywheel remains intact

- Semiconductors have become the purest expression of that spend, with NVIDIA and peers capturing the upside while the rest of the market lags

- The risk is not demand, it is the rate of change in capex, flat spending in a rising cost world is effectively a slowdown and a direct threat to current positioning

- Market breadth is thin and concentration extreme; you are either inside the AI supply chain or you are not participating, leaving the tape vulnerable if the narrative even slightly loses momentum

Equities Driven By AI Spend

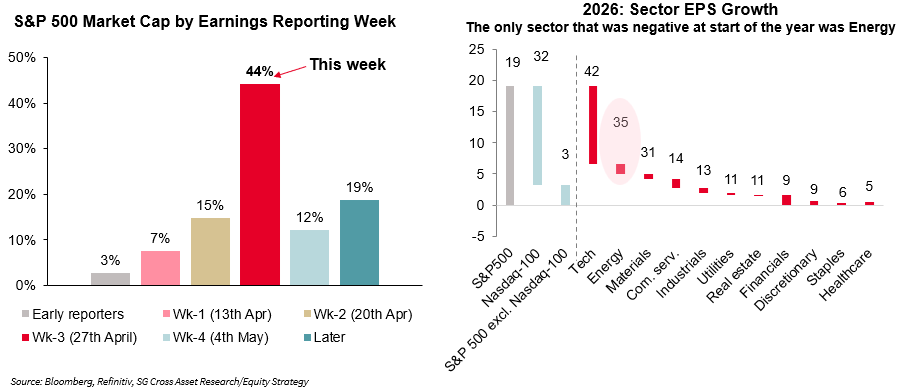

This is the week where the tape stops trading mood music and starts trading hard proof. As previewed earlier, profits and policy are now landing on the same runway, with every G5 central bank stepping up to the microphone just as Hormuz negotiations continue to flicker across the headline tape. More than 42% of the reports this week, representing roughly $29 trillion in market cap, which means this is not just earnings season anymore. It is a full market stress test, where AI optimism, rate expectations, oil risk, and geopolitical hope all get marked to market in real time..

…and Wednesday is where it all compresses into a single point of impact. One of the most concentrated earnings sessions in market history, measured by sheer percentage of index market cap reporting in a single window. This is not a drip-fed information; it is a liquidity event disguised as a calendar entry. , , and all hit after the close, effectively forcing the entire AI complex to mark its books in one coordinated print. Then Apple walks in a day later, less as a follow-up and more as the final calibration of whether the consumer side of the equation can still carry the weight.

This is where concentration risk stops being a slow burn and becomes an event. The generals are reporting at the same time, and when that happens the market does not get the luxury of narrative drift. It gets repriced, clean and immediate, in the cold light of realized earnings versus the expectations that have been doing all the heavy lifting.

That day is not about the headline EPS beats or misses; it is about the plumbing behind the story. It is where the market digs into forward capex guidance to see whether the AI narrative is still being funded at full throttle or quietly being rationed. The tape knows the number, more than $740Bn in AI capex already signposted for 2026, but what it does not know is whether that number holds, expands, or starts to leak at the margins.

When Alphabet, Microsoft, Amazon and Meta Platforms open the books, they are not just reporting earnings; they are effectively underwriting the next leg of the cycle. Capex is the oxygen in this trade. If those commitments stay intact or, more importantly, get pushed higher, the market reads that as validation that the AI buildout is still in land grab mode, and multiples can justify their altitude.

But if there is even a hint of hesitation, a subtle shift from aggressive expansion to capital discipline, the entire complex has to reprice. Because this rally has not been built on what AI is today, it has been built on what it is expected to become, and that expectation is financed through capex. Cut the fuel line, even slightly, and the coiled spring in positioning does not unwind gently; it snaps.

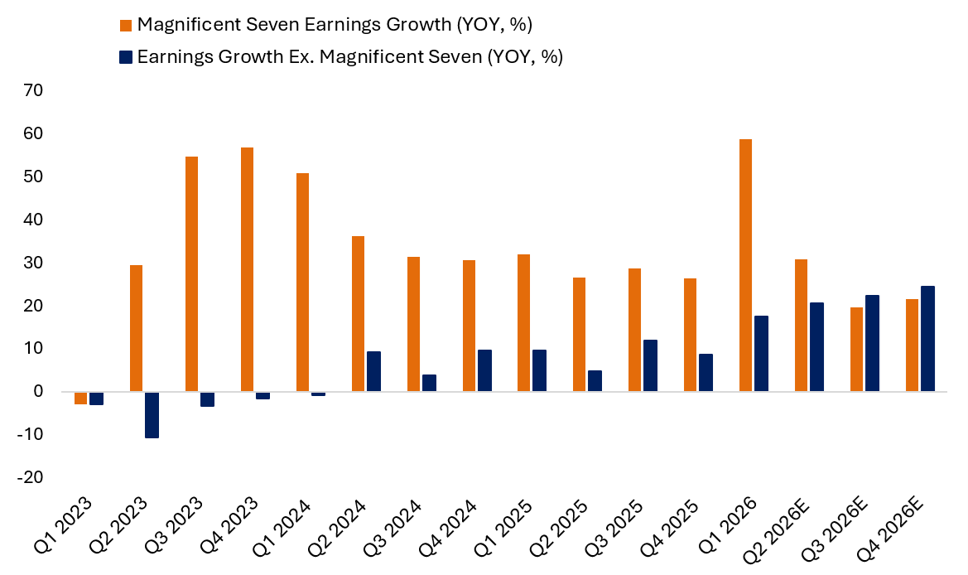

Semiconductors are no longer just part of the story, they are the transmission mechanism. The direct beneficiaries of that capex torrent, and right now the cleanest expression of where the money is actually flowing. Year to date they have run 42%, leaving the so-called leadership cohort looking almost stationary, with the Mag 7 barely scraping +2% and ex NVIDIA (NASDAQ:) effectively flat. Strip away the narrative, and what you are left with is a market where the picks and shovels have dramatically outperformed the gold miners.

Put differently, roughly 40% of S&P 500 Growth in 2026 is being driven by semiconductors, and that growth is not organic in the traditional sense; it is being pulled forward by the capex commitments of the very same hyperscalers reporting this week. Microsoft, Amazon, Alphabet and Meta Platforms are effectively writing the revenue line for the chip complex in advance.

This is where the feedback loop becomes critical. Capex drives semiconductor demand, semiconductor performance drives index returns, and index performance reinforces the belief that the capex is justified. It is a self-sustaining flywheel until it is not. Because the moment that capex guidance even wobbles, the first place the market looks is not at the platforms, it is at the suppliers. And in a tape this concentrated, where one segment is doing the heavy lifting for the entire growth complex, any disruption to that flow does not diffuse. It cascades.

What you are seeing beneath the surface is not a broad earnings recovery, it is a concentration trade masquerading as one. Since the war kicked off, the upward revisions to S&P 500 earnings have not been a rising tide lifting all boats; they have been a handful of supertankers dragging the index higher while the rest of the fleet drifts.

At the center of that move sits Micron Technology (NASDAQ:), which alone has accounted for more than half of the total upward EPS revision. That is not incremental improvement; that is a step change, with consensus estimates effectively doubling after a print and guide that blew past expectations, all anchored in the belief that memory demand tied to the AI supercycle is not just strong but insatiable. In second place is Exxon Mobil (NYSE:), contributing roughly 14% of the revision, a reminder that while AI is the narrative, energy is still the pricing engine sitting underneath inflation and margins.

Everything else tells a very different story. The median S&P 500 name has seen little to no change in estimates. No surge, no broad upgrade cycle, just a flatline. That is the tell. Because when earnings revision breadth narrows like this, the index starts to behave less like a diversified portfolio and more like a levered position in a few dominant themes.

From my seat, the market is no longer being carried by a chorus; it is being carried by a soloist with a very loud microphone. And that works, right up until the moment the voice cracks.

Take a step back and the bigger picture snaps into focus. Strip out the noise of weekly flows and headline roulette, and what you see over the past five years is a market where virtually all earnings growth and margin expansion has been carried on the shoulders of tech. Not supported by, not complemented by, but outright driven by it.

The rest of the index has been along for the ride, at times stabilizing, occasionally contributing, but never truly leading. The heavy lifting, the multiple expansion, the margin resilience in the face of inflation shocks, rate cycles, and geopolitical stress, has all come from the same core engine. Microsoft, Alphabet, Amazon, Meta Platforms, and increasingly NVIDIA have not just participated in growth, they have defined it.

Which leaves the market in a very specific place. This is no longer a diversified earnings cycle; it is a single-engine aircraft flying at altitude. As long as that engine continues to fire, the ride is smooth, even elegant. But it also means there is very little redundancy in the system. Because when all earnings and margin expansion trace back to one part of the market, that part stops being the leader. It becomes systemic.

And that is the quiet risk embedded in the charts. Not that tech has driven the last five years, but that it has been the only thing that has.

It all comes back to the same axis. Tech, capex, and the belief that the spigot stays wide open. As long as the hyperscalers keep writing ever larger checks, the market can keep telling itself the story holds. But peel that back, and the plumbing looks more complicated.

The big picture, as framed by Goldman’s Delta One desk, is brutally simple. Equities are being driven by one thing: AI spend. Everything else is orbiting around it. What is emerging beneath that is more like an arms race than a rational allocation of capital. Engineering teams are effectively “token maxing,” competing to consume as much compute as possible, because under-spending is no longer prudent; it is a career risk. That creates a system in which capital is deployed aggressively, sometimes inefficiently, but always with the same objective: not to fall behind.

And yet the constraints are already visible. Power grids are tight, GPUs are scarce, CPUs are spoken for, copper is suddenly strategic again, and even qualified engineers are a bottleneck. The physical world is pushing back against the digital ambition. But the market, for now, is choosing to look straight through it, extrapolating a clean line higher. More tokens, more intelligence, and eventually something that starts to resemble AGI.

In the here and now, it is hard to argue with the tape. Supply is constrained, earnings are accelerating, and the narrative, whether fully justified or not, carries the weight of a generational shift. That is enough to keep the bid intact. But this is where the tension builds.

This week’s earnings compress that tension into a single moment. Amazon, Microsoft, Meta Platforms and Alphabet all report into a market that already has enormous 2026 capex baked in, north of $600Bn across the group. The question is no longer whether demand is strong. That part is settled. The question is whether the spending curve steepens again.

Because if capex merely holds flat in a world where input costs are rising, that is not stability; it is a slowdown in disguise. And that is where the fault line runs between the suppliers and the spenders. The semiconductor complex has been priced as a direct call option on ever-rising capex. The hyperscalers themselves have not been rewarded in the same way for writing those checks. One side is infatuated with spending. The other is starting to question the return on it.

So you end up with a market that has been almost entirely powered by AI spend. That is the source of the upside surprise, the driver of earnings revisions, the engine behind the rally. Aside from that, the oxygen is thin. Energy prices are creeping back into the inflation narrative, Europe is lagging, and dispersion is extreme. You are either inside the AI supply chain, or you are watching from the outside.

From here, the setup shifts. The strength of the AI bid is undeniable, but the velocity has been extreme. What was a tailwind in positioning and technicals is starting to turn. When everything is priced off one variable, the risk is not that it disappears, it is that it stops accelerating. And in this tape, that alone is enough to change the direction of travel.

Asia Open: Oil Climbs & Asia Rally Gets Tested

Takeaways

- Oil strength is no longer background noise, it is the pressure point that can destabilize the entire risk rally

- The equity market is being carried by a narrow group of megacap names whose earnings now define the next directional move

- Central banks face a growing tension between maintaining patience and responding to rising energy-driven inflation risk

Asia Rally Gets Tested

The market has been drifting higher on a soft current of relief, the kind that feels calm on the surface but carries a quiet undertow. Now the tide is shifting. closing at $108.23 after a six-day climb is not just another print; it is the market clearing its throat, reminding anyone willing to listen that the energy story has not gone away, it has simply been pushed to the edge of the stage. at $96.66 keeps that rhythm intact, a steady drumbeat beneath the melody of rising equities.

Asia has retraced its steps with discipline, walking back the war losses and returning to levels last seen before the February escalation. MSCI Asia now stands where it once stood before the first shots were fired, as if the market has chosen to remember calm rather than conflict. But futures are hesitating, mixed and searching, like a trader hovering over the keyboard, waiting for one more piece of information before committing capital.

In currency markets, the yen holds steady ahead of the Bank of Japan decision, neither leaning in nor pulling back, just holding its breath. Rates echo the same restraint. Treasury yields have edged higher, but remain locked inside one of the tightest monthly ranges since 2020. It is a market that has compressed its uncertainty into a narrow band, waiting for something to force it open.

Equities have found their lift elsewhere. The artificial intelligence trade has returned like a familiar refrain, pulling the S&P toward its strongest month since 2020. But the strength is narrow, concentrated, almost theatrical. A handful of megacap names are carrying the weight of the entire structure, and now they step forward into the light. Alphabet (GOOGL), Microsoft (MSFT), Amazon (AMZN), Meta (META), and Apple (AAPL), together nearing $16 trillion in value, are not simply reporting earnings, they are being asked to justify the story itself. If they deliver, the music plays on. If they falter, the stage goes quiet very quickly.

There are already faint signs of strain. The semiconductor complex, after a historic ascent, has begun to ease. Not a collapse, not even a correction, just a softening at the edges. But in markets like this, the edges matter. They are where momentum begins to fray.

Geopolitics remains the shadow cast across all of it. Washington is engaging with Tehran’s latest proposal, one that hints at reopening Hormuz in exchange for relief from pressure. It is a negotiation wrapped in conditions, progress layered with doubt. One side testing the boundaries, the other holding its line. The language suggests movement, but not resolution, like two counterparties circling agreement without quite closing the trade.

From the trading desk, the shift is subtle but decisive. The market is no longer reacting to each headline; it is reacting to expectations about how those headlines resolve. That changes everything. When probability replaces immediacy, positioning begins to lean, and when positioning leans, the balance becomes fragile. It is not the base case that hurts; it is the surprise that was never priced.

Central banks now enter this delicate composition. The Federal Reserve, the European Central Bank, and peers across Japan, the UK, and Canada are all stepping to the microphone in the same week. No one expects movement on rates. The real signal will come in tone, in cadence, in how they speak about oil, inflation, and the risk that expectations begin to drift.

The tension is building. Policymakers want to wait, to observe, to keep their options open. But the market is beginning to press for clarity. Energy is rising, equities are elevated, and the gap between the two is narrowing. That gap does not stay open for long. It resolves, and when it does, it rarely does so quietly.

This rally has been built on a delicate alignment. Earnings strength, carrying valuations, geopolitics fading into the background, and inflation contained just enough to keep policy steady. Now each of those pillars is being tested at the same time. Oil is rising, earnings are about to be revealed, and central banks are being forced to speak into the tension.

This is no longer a market climbing a wall of worry. It is a market gliding across a frozen surface, smooth and confident, but dependent on the integrity of what lies beneath. Oil is the first crack. Earnings are the weight pressing down. Policy is the temperature that decides whether the ice holds or gives way.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.